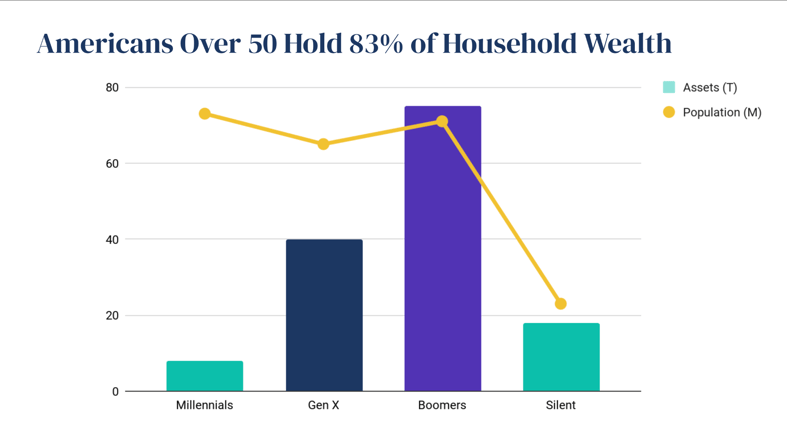

Americans over 50 are the wealthiest generation in US history. They control 83% of US household wealth making them credit unions’ most valuable member segment today. Goldman Sachs reports that this huge generation has an estimated $30 trillion to transfer to successor generations, who largely don’t belong to a credit union.

At Curql Collective, we have been encouraged by the response of many credit unions to mitigate the $30T deposit flight risk by improving their digital experiences, expanding offerings, and acquiring younger members. However, if credit unions don’t focus on their current Baby Boomer members, they will not address the transfer risk and tragically miss out on capturing the $70T retirement wallet opportunity that is under their noses. As you reevaluate your credit union’s strategy, consider some eye-opening insights from our portfolio company, Silvur.

Understanding The Over-50 Crowd

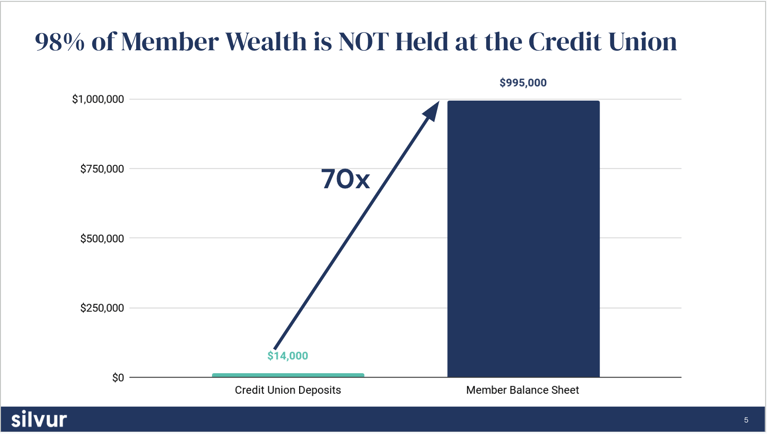

Within credit unions’ existing membership lies tremendous untapped opportunity. Silvur estimates that for every $10,000 held at credit unions, Baby Boomers have $700,000 in assets held away at other financial institutions – a total retirement wallet of $70 trillion, making them credit unions’ most valuable member segment.

Baby Boomers are living 10 years longer and will continue to hold the lion’s share of US wealth for 20-30 more years. Credit unions need to refocus their strategies and investments to retain and delight this segment. Acquiring younger members is a critical long-term goal but evolving existing business lines and solutions for the needs of the 50+ demographic is immediately achievable, represents a larger asset opportunity, and is much more capital efficient.

Risk of Account Consolidation

During retirement Americans consolidate and simplify every aspect of their lives. Multiple 401(k) accounts are rolled into a single traditional individual retirement account (today 6 in 10 American households with IRAs have rollovers). The same is true of a member’s financial institution. Credit unions can either invest in these members or get consolidated out of the game long before the wealth transfer takes place.

Tactics for Serving Through the Transfer

As a fintech specializing in retirement solutions, Silvur has sage advice for credit unions that want to avoid these risks and miss out on opportunities.

Above all, credit unions should reinforce their positions as primary financial institutions for this demographic, which is the largest buyer segment for homes, boats, RVs, and cars. They have the most wealth and are much less rate-sensitive; this demographic is more likely to downsize rather than delay due to high rates.

One sure way to strengthen your PFI status is to help your members navigate the decisions they must make in retirement. With Silvur you can offer members an always-on technology solution that delivers high-quality education about social security, Medicare, taxes, and other critical decisions they must make during this phase of life. Silvur’s proprietary Retirement Score provides a metric of how long each member’s assets will last in retirement. This is the most reported anxiety and the most difficult question for an individual to answer. Additionally, Silvur can share member data and insights to tailor your products and services to this critical member segment’s needs.

Refocusing existing business lines can meet your members’ needs while opening more opportunities for credit union growth. In the short term, retirees are a fantastic target market for lending products as mentioned above. Additionally, deposit campaigns can encourage bringing in required minimum distributions from retirement accounts, while pitching certificates of deposit, high-yield savings accounts, and money market accounts to offer members age 62+ the security they seek for their nest eggs.

For longer-term growth, focus on wealth management and Medicare opportunities. Wealth management typically only reaches 1 – 2% of members, so there are opportunities to grow this business line by identifying and pursuing higher funnel opportunities using Silvur’s data and insights. The annual IRA rollover opportunity in the US is a hefty $765 billion. Additionally, consider guiding members through their health decisions in retirement. Medicare is both complex and an enormous cost, and the annual registration requirement ensures regular touchpoints with your members.

Your 2024 Priority

One simple way to get started is to focus on promoting direct deposit among members age 62+ for both payroll and retirement income such as Social Security, annuities, and pensions. $1 trillion in social security payments is directly deposited to retirees every year, and credit unions that don’t make the transition from W2 to social security direct deposit are at grave risk of losing PFI status and getting “consolidated out.”

By taking advantage of Silvur's offerings, credit unions can also increase operational efficiency and gain easy access to data to improve your marketing and conversion for your most valuable demographic. With plug-and-play activation, it is easy to get started with Silvur, and no additional resources are needed.

Learn more about capturing opportunities throughout the ongoing wealth transfer at silvur.com.